In this chapter we discuss the provisions incorporated in a policy document. The provisions discussed in the chapter include some important provisions related to grace period, policy lapse and non-forfeiture etc.

A. Policy conditions and privileges

1. Grace period

Every life insurance contract undertakes to pay the death benefit on the condition that the premiums have been paid up to date and the policy is in force. The “Grace Period” clause grants the policyholder an additional period of time to pay the premium after it has become due.

The standard length of the grace period is one month or 31 days. The days of grace may be computed from the next day after the due date fixed for payment of the premium. The provision enables a policy that would otherwise have lapsed for non-payment of premium, to continue in force during the grace period.

The premium however remains due and if the policyholder dies during this period, the insurer may deduct the premium from the death benefit. If premiums remain unpaid even after the grace period is over, the policy would then be considered lapsed and the company is not under obligation to pay the death benefit. The only amount payable would be whatever is applicable under the non-forfeiture provisions. In a sense the insured may thus be said to have received free insurance during the grace period.

2. Lapse and Reinstatement / Revival

We have already seen that a policy may be said to be in lapse condition if premium has not been paid even during the days of grace. The good news is that practically all the permanent life insurance contracts permit reinstatement (revival) of a lapsed policy.

Reinstatement is the process by which a life insurance company puts back into force a policy that has either been terminated because of non-payment of premiums or has been continued under one of the non-forfeiture provisions.

A revival of the policy cannot however be an unconditional right of the insured. It can be accomplished only under certain conditions:

i. No increase in risk for insurer: Revival of a policy cannot result in an increase in risk for the insurance company

ii. Creation of reserve: The policyholder must pay such amount of premiums with interest, as would lead to creation of the same reserve it would have accumulated if the policy had not lapsed.

iii. Revival application within specific time period: The policy owner must complete the revival application within the time frame stated in the provision for such reinstatement. In India revival must be affected within a specific time period, say five years, from the date of lapse.

iv. Satisfactory evidence of continued insurability: The insured must present to the insurance company satisfactory evidence of continued insurability of the insured. Not only must her health be satisfactory but other factors such as financial income and morals must not have deteriorated substantially.

v. Payment of overdue premiums with interest: The policy owner is required to make payment of all overdue premiums with interest from due date of each premium.

vi. Payment of outstanding loan: The insured must also pay any outstanding policy loan or reinstate any indebtedness that may have existed.

The company may however require a medical examination or other evidence of insurability under certain circumstances:

i. One is where the grace period has expired since long and the policy is in a lapsed condition for say, nearly a year.

ii. Another situation is where the insurer has reason to suspect that a health or other problem may be present. Fresh medical examination may also be required if the sum assured or face amount of the policy is large.

Since a revival may require the policyholder to pay a sizeable sum of money (past arrears of premium and interest) for the purpose, each policyholder must decide whether it would be more advantageous to revive the original policy or purchase a new policy. Revival is often more advantageous because buying a new policy would call for a higher premium rate based on the age the insured has attained on date of revival.

a) Policy revival measures

Let us now look at some of the ways through which policy revival can be accomplished. In general one can revive a lapsed policy if the revival is within a certain period (say 5 years) from the date of first unpaid premium.

i. Ordinary revival

The simplest form of revival is one that involves payment of arrears of premium with interest. This has been termed as ordinary revival and is affected when the policy has acquired surrender value. The insurer would also call for a declaration of good health or some other evidence of insurability like a medical examination.

ii. Special revival

What do we do when the policy has run for less than three years and has not acquired minimum surrender value (i.e. the accumulated reserves or cash value is insignificant) but the period of lapse is large?, say the policy is coming up for revival after a period of one year or more since the date of first unpaid premium.

One way to revive it is through a scheme known as special revival (which is for instance prevalent in LIC of India). Here it is as though a new policy has been written, whose date of commencement is within two years of the original date of commencement of the lapsed policy. The maturity date shall not exceed the original stipulated period as applicable to certain lives at the time of taking the policy.Example

If the original policy was taken at age 40 and the new date of commencement is at age 42, the term of the policy may now be reduced from twenty to eighteen for those policies that require that the term should end at age 60. Difference between old and new premium with interest thereon has to be paid.

iii. Loan cum revival

Yet a third approach to revival also available with LIC and other companies is that of loan cum revival. This is not a revival alone but involves two transactions:

• the simultaneous granting of a loan and

• revival of the policyArrears of premium and interest are calculated as under ordinary revival. The loan that one is eligible to get under the policy as on date of revival is also determined. This loan may be utilised as consideration amount for revival purposes. If there is any balance amount subsisting after loan adjustment towards arrears of premium and interest, it is payable to the policyholder. Obviously, the facility of loan cum revival would be allowed only for policies that have acquired surrender value as on date of revival.

iv. Instalment revival

Finally we have instalment revival which is allowed when the policyholder is not in a position to pay arrears of premium in a lump sum and neither can the policy be revived under special revival scheme. The arrears of premium in such case would be calculated in the usual manner as under an ordinary revival scheme.

Depending on the mode of payment (quarterly or half yearly) the life assured may be required to pay one half yearly or two quarterly premiums. The balance of arrears to be paid would then be spread so as to be paid with future premiums on premium due dates, during a period of two years or more, including the current policy anniversary yearand two full policy anniversaries thereafter. A condition may be imposed that there should be no outstanding loan under the policy at the time of revival.

Revival of lapsed policies is an important service function that life insurers seek to actively encourage since policies in lapsed state may do little good to either insurer or policyholder.

3. Non-forfeiture provisions

One of the important provisions under the Indian Insurance Act (Section 113) is that which allows for accrual of certain benefits to policyholders even when they are unable to keep their policies in full force by payment of further premiums. The logic, which applies here, is that the policyholder has a claim to the cash value accumulated under the policy.

a) Surrender values

Life insurers normally have a chart that lists the surrender values at various times and also the method that will be used for calculating the surrender values. The formula takes into account the type and plan of insurance, age of the policy and the length of the policy premium-paying period. The actual amount of cash one gets in hand on surrender may be different from the surrender value amount prescribed in the policy.

This is because paid up additions, bonuses or dividend accumulations, advance premium payments or gaps in premiums, policy loans etc. may result in additions or subtractions from the cash surrender value accrued. What the policyholder ultimately receives is a net surrender value.Surrender Value is a percentage of paid-up value.

Surrender Value arrived as a percentage of premiums paid is called

Guaranteed Surrender Value.

b) Policy loans

Life insurance policies that accumulate a cash value also have a provision to grant the policyholder the right to borrow money from the insurer by using the cash value of the policy as a security for the loan. The policy loan is usually limited to a percentage of the policy’s surrender value (say 90%). Note that the policyholder borrows from his own account. He or she would have been eligible to get the amount if the policy had been surrendered.

In that case however the insurance would also have been terminated. By instead taking a loan on the policy, a policyholder is able to keep the cake and eat it too. A loan provides access to liquid funds while keeping the insurance alive. A loan is what you would recommend to a client in need of urgent funds but you would like to keep him or her as your client.

A policy loan is different from an ordinary commercial loan in two respects:

Policy loan |

Commercial loan |

No legal obligation to repay the loan: The policy owner is not legally obligated to repay the loan. She can repay all or part of the loan at any time she chooses. If the loan has not been repaid, the insurer deducts the amount of outstanding (unpaid) loan and interest from the policy benefit that is payable. |

A commercial loan creates a debtor – creditor relationship in which the borrower is legally obligated to repay the lender. |

No credit check is required: Since the insurer does not really lend its own funds to the policyholder, it is not necessary to perform a credit check on the debtor when the latter applies for the loan. The insurer needs to only |

The creditor does a thorough credit check on the debtor |

ensure that the loan does not exceed the eligible amount (90% of SV as suggested above).

The insurer off course reserves the right to decide on terms and conditions of such loans from time to time as a matter of policy. Since the loan is granted on the policy being kept as security, the policy has to be assigned in favour of the insurer. Where the policyholder has nominated someone to receive the money in the event of death of the insured, this nomination shall not be cancelled by the subsequent assignment of the policy.

The nominee’s right will affected to the extent of the insurer’s interest in the policy.

Arjun bought a life insurance policy wherein the total death claim payable under the policy was Rs. 2.5 lakhs. Arjun’s total outstanding loan and interest under the policy amounts to Rs. 1.5 lakhs

Hence in the event of Arjun’s death, the nominee will be eligible to get the balance of Rs. 1 lakh

Insurers usually charge interest on policy loans, which are payable semi-annually or annually. If the interest charges are not paid they become part of the policy loan and are included in the loan outstanding.

So long as the premiums are paid in time and the policy is in force, the accumulated cash value will generally be more than sufficient to pay for the loan and interest charges. But if the policy is in a lapsed condition and no new premiums are forthcoming a situation can arise where the amount of outstanding loan plus unpaid interest (the total debt) becomes greater than the amount of policy’s cash value.

The insurer obviously cannot allow such a situation. Well before such an eventuality, insurers generally take what is termed as foreclosure action. Notice is to be given to the policyholder before the insurance company resorts to foreclosure. The policy is terminated and subsisting cash value is adjusted to loan and interest that is outstanding. Any excess amount may be paid to the policyholder.

4. Special policy provisions and endorsements

a) Nomination

i. Nomination is where the life assured proposes the name of the person(s) to whom the sum assured should be paid by the insurance company after their death.

ii. The life assured can nominate one or more than one person as nominees.

iii. Nominees are entitled for valid discharge and have to hold the money as a trustee on behalf of those entitled to it.

iv. Nomination can be done either at the time the policy is bought or later.

v. Under Section39 of the Insurance Act 1938, the holder of a policy on their own life may nominate the person or persons to whom the money secured by the policy shall be paid in the event of their death.

Nomination can be changed by making another endorsement in the policy.

Nomination only gives the nominee the right to receive the policy monies in the event of the death of the life assured. A nominee does not have any right to the whole (or part) of the claim.

Where the nominee is a minor, the policy holder needs to appoint an appointee. The appointee needs to sign the policy document to show his or her consent to acting as an appointee. The appointees lose their status when the nominee reaches majority age. The life assured can change the appointee at any time. If no appointee is given, and the nominee is a minor, then on the death of the life assured, the death claim is paid to the legal heirs of the policyholder.

Where more than one nominee is appointed, the death claim will be payable to them jointly, or to the survivor or survivors. No specific share for each nominee can be made. Nominations made after the commencement of the policy have to be intimated to the insurers to be effective.

Diagram 1: Provisions related to nomination

b) Assignment

The term assignment ordinarily refers to transfer of property by writing as distinguished from transfer by delivery. The ownership of property consists of various rights in respect of such property, which are vested in one or more persons.

On assignment, nomination is cancelled, except when assignment is made to insurance company for a policy loan.

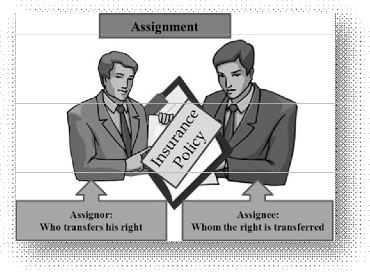

The assignment of a life insurance policy implies the act of transferring the rights right, title and interest in the policy (as property) from one person to another. The person who transfers the rights is called assignor and the person to whom property is transferred is called assignee.

Diagram 2: Assignment

In India assignment is governed by Section 38 of Insurance Act. On execution of the assignment the assignee gets all rights title and interest in respect of property assigned and becomes the owner of the policy, subject to the provision that the assignee cannot have a better title than the assignor.

This last provision is very important. It means simply that the assignee would not be eligible to get a claim that for some reason is rejected to the assured. Assignment requires that the parties be competent to contract and is not subject to legal disqualifications.

There are two types of assignments.

Diagram 3: Types of Assignment

Conditional Assignment |

Absolute Assignment |

Conditional assignment provides that the policy shall revert back to the life assured on his or her surviving the date of maturity or on death of the assignee. |

Absolute assignment provides that all rights, title and interest which the assignor has in the policy are transferred to the assignee without reversion to the former or his/her estate in any event. The policy thus vests absolutely with the assignee. The latter can deal with the policy in whatever manner he or she likes without the consent of the assignor. |

Absolute assignment is more commonly seen in many commercial situations where the policy is typically mortgaged against a debt assumed by the policyholder, like a housing loan.

Let us now look at the conditions that are necessary for a valid assignment.

i. First of all the person executing it (the assignor) must have absolute right and title or assignable interest to the policy being assigned.

ii. Secondly it is necessary that the assignment be supported by valuable consideration, which may include love and affection.

iii. Thirdly it is imperative that the assignment is not opposed to any law in force. For example the assignment of a policy to a foreign national residing in another country may contravene exchange control regulations.

iv. Assignee can do another assignment, but cannot do nomination because assignee is not the life assured.

The assignment has to be in writing and must be signed and attested by at least one witness. The fact of transfer of title has to be specifically set forth in the form of an endorsement on the policy. It is also necessary that the policyholder must give notice of the assignment to the insurer. Unless such notice in writing is received by the insurer, the assignee would not have any right of title to the policy.

On receipt of the policy document for endorsement and notice the life insurance may affect and register the assignment. It must be noted that while registering the assignment the company does not take any responsibility or express any opinion about its validity or legal effect. The date of the assignment as recorded in the books of the life insurance company would be the date on which the assignment and notice thereof has been received by its concerned office. If the notice and the assignment were to be received on separate dates, the date of the one received later will be deemed as the date of registration.

An assignee may reassign interest in the policy to the policyholder /life assured during the currency of the policy. On such reassignment the latter may be advised to execute a fresh nomination or assignment for expeditious settlement of the claim. Again, in the case of conditional assignment the title to the policy would revert to the life assured in the event of death of the assignee. On the other hand if the assignment were absolute, the title would pass to the estate of the deceased assignee.

Diagram 4: Provisions related to assignment of insurance policies

Basis of Difference |

Nomination |

Assignment |

What is Nomination or Assignment? |

Nomination is the process of appointment of a person to receive the death claim |

Assignment is the process of transferring the title of the insurance policy to another person or institution. |

When can the nomination or assignment be done? |

Nomination can be done either at the time of proposal or after the commencement of the policy. |

Assignment can be done only after commencement of the policy. |

Who can make the nomination or assignment? |

Nomination can be made only by the life- assured on the policy of his own life. |

Assignment can be done by owner of the policy either by the life assured if he is he policyholder or the assignee |

Where is it applicable? |

It is applicable only where the Insurance Act, 1938 is applicable. |

It is applicable all over the world, according to the law of the respective country relating to transfer of property. |

Does the policyholder retain control over the policy? |

The policyholder retains title and control over the policy and the nominee has no right to sue under the policy |

The policyholder loses the right, title and interest under the policy until a re-assignment is executed and the assignee has a right to sue under the policy. |

Is a witness required? |

Witness is not required. |

Witness is mandatory. |

Do they get any rights? |

Nominee has no rights over the policy. |

Assignee gets full rights over the policy, and can even sue under the policy. |

Can it be revoked? |

Nomination can be revoked or cancelled at any time during the policy term. |

The assignment once done cannot be cancelled, but can be re- assigned. |

In case of minor: |

In case the nominee is a minor, appointee has to be appointed. |

In case the assignee is a minor, a guardian has to be appointed. |

What happens in |

In case of nominee’s |

In case of conditional |

case of the nominee’s or assignee’s death? |

death, the rights of the policy revert to the policyholder or to his legal heirs. |

assignee’s death, the rights on the policy revert back to the life assured, based on the terms of assignment. In case of the absolute assignee’s death, his legal heirs are entitled to the policy. |

What happens in case of death of the nominee or assignee after the death of the life- assured and before the payment of the death claim |

In case the nominee dies before the settlement of death claim, the death claim will be payable to the legal heirs of the life assured. |

In case the assignee dies before the settlement, the policy money is payable to the legal heirs of the assignee and not the life-assured who is the assignor. |

Can creditors attach the policy? |

Creditors can attach the insurance policy which has a nomination in it. |

Creditors cannot attach the policy unless the assignment is shown to have been made to defraud the creditors. |

c) Duplicate Policy

A life insurance policy document is only an evidence of a promise. Loss or destruction of the policy document and does not in any way absolve the company of its liability under the contract. Life insurance companies generally have standard procedures to be followed in case of loss of the policy document.

Normally the office would examine the case to see if there is any reason to doubt the alleged loss. Satisfactory proof may require to be produced that the policy has been lost and not been dealt with in any manner. Generally the claim may be settled on the claimant furnishing an indemnity bond with or without surety.

If payment is shortly due and the amount to be paid is high, the office may also insist that an advertisement be placed in a national paper with wide circulation, reporting the loss. A duplicate policy may be issued on being sure that there is no objection from anyone else.

d) Alteration

Policyholders may seek to effect alterations in policy terms and conditions. There is provision to make such changes subject to consent of both the insurer and assured. Normally alterations may not be permitted during the first year of the policy, except for change in the mode of premium or alterations which are of a compulsory nature – like

• change in name or / address;

• readmission of age in case it is proved higher or lower;

• request for grant of double accident benefit or permanent disability benefit etc.

Alterations may be permitted in subsequent years. Some of these alterations may be affected by placing a suitable endorsement on the policy or on a separate paper. Other alterations, which require a material change in policy conditions, may require the cancellation of existing policies and issue of new policies.

Some of the main types of alterations that are permitted are

i. Change in certain classes of insurance or term [where risk is not increased]

ii. Reduction in the sum assured

iii. Change in the mode of payment of premium

iv. Change in the date of commencement of the policy

v. Splitting up of the policy into two or more policies

vi. Removal of an extra premium or restrictive clause

vii. Change from without profits to with profits plan

viii. Correction in name

ix. Settlement option for payment of claim and grant of double accident benefit

These alterations generally do not involve an increase in the risk. There are other alterations in policies that are not allowed. These may be alterations that have the effect of lowering the premium. Examples are extension of the premium paying term; change from with profit to without profit plans; change from one class of insurance to another, where it increases the risk: and increase in the sum assured.

Insurance companies everywhere are generally allowed to select the actual wording of their policy documents, but these may need to be submitted to the regulator for approval.

Under what circumstances would the policyholder need to appoint an appointee?

I. Insured is minor

II. Nominee is a minor

III. Policyholder is not of sound mind

IV. Policyholder is not married

• The grace period clause grants the policyholder an additional period of time to pay the premium after it has become due.

• Reinstatement is the process by which a life insurance company puts back into force a policy that has either been terminated because of non- payment of premiums or has been continued under one of the non- forfeiture provisions.

• A policy loan is different from an ordinary commercial loan in two respects, firstly the policy owner is not legally obligated to repay the loan and the insurer need not perform a credit check on the insured.

• Nomination is where the life assured proposes the name of the person(s) to which the sum assured should be paid by the insurance company after their death.

• The assignment of a life insurance policy implies the act of transferring the rights right, title and interest in the policy (as property) from one person to another. The person who transfers the rights is called assignor and the person to whom property is transferred is called assignee.

• Alteration is subject to consent of both the insurer and assured.

Normally alterations may not be permitted during the first year of the

policy, except for some simple ones.

1. Grace period

2. Policy lapse

3. Policy revival

4. Surrender value

5. Nomination

6. Assignment