In India, as per the IRDA norms, there are thus only two kinds of non-traditional savings life insurance products that are permitted:

The chapter introduces you to the world of non-traditional life insurance products. We start by examining the limitations of traditional life insurance products and then have a look at the appeal of non-traditional life insurance products. Finally we look at some of the different types of non-traditional life insurance products available in the market.

A. Overview of non-traditional life insurance products

B. Non-traditional life insurance products

1. Non-traditional life insurance products – Purpose and need

In the previous chapters we have considered some of the traditional life insurance products which have insurance as well as a savings element in them. These products have often been considered as being part of the financial market and compared with other instruments of capital accumulation.

One of the principal purposes of saving and investing, we must note, is to achieve inter-temporal allocation of resources, which is both efficient and effective.

i. Inter-temporal allocation means allocation across time. The term effective here implies that sufficient funds are available to successfully satisfy various needs as they arise in different stages of the life cycle.

ii. Efficient allocation on the other hand implies a faster rate of accumulation and more funds available in future. Higher the return for a given level of risk, the more efficient would the investment be.

2. Limitations of traditional products

A critical examination would reveal the following areas of concern:

a) Cash value component: Firstly, the savings or cash value component in such policies is not well defined. It depends on the amount of actuarial reserve that is set up. This in turn is determined by assumptions about mortality, interest rates, expenses and other parameters that are set by the life insurer. These assumptions can be quite arbitrary.

b) Rate of return: Secondly it is not easy to ascertain what would be rate of return on these policies. This is because the value of the benefits under “With Profit policies” would be known for sure, only when the contract comes to an end. Again, the exact costs of the insurer are not disclosed. This lack of clarity about the rate of return makes it difficult to compare them with other alterative instruments of savings. Obviously one cannot know how efficient life insurance is as a savings instrument unless one can make such comparison.

c) Surrender value: A third problem is that the cash and surrender values (at any point of time), under these contracts depend on certain values (like the amount of actuarial reserve and the pro-rata asset share of the policy). These values may be determined quite arbitrarily. The method of arriving at surrender value is not visible.

d) Yield: Finally there is the issue of the yield on these policies. Both because of prudential norms and tight supervision on investment and because bonuses do not immediately reflect the investment performance of the life insurer, the yields on these policies may not be as high as can be obtained from more risky investments.

3. The shifts

As the limitations of traditional life insurance plans became obvious, a number of shifts occurred in the product profiles of life insurers. These have been summarised below:

a) Unbundling

This trend involved separation of the protection and savings elements and consequently the development of products, which stressed on protection or savings, rather than a vague mix of both.

While in markets like the United States, these led to a rediscovery of term insurance and new products like universal assurance and variable assurance, the United Kingdom and other markets witnessed the rise of unit linked insurance.b) Investment linkage

The second trend was the shift towards investment linked products, which linked benefits to policyholders with an index of investment performance. There was consequently a shift in the way life insurance was positioned. The new products like unit linked implied that life insurers had a new role to play. They were now efficient fund managers with the mandate of providing a high competitive rate of yield, rather than mere providers of financial security.

c) Transparency

Unbundling also ushered greater visibility in the rate of return and in the charges made by the companies for their services (like expenses etc.). All these were explicitly spelt out and could thus be compared

d) Non-standard products

The fourth major trend has been a shift from rigid to flexible product structures, which is also seen as a move towards non-standard products. When we speak of non–standard, it is with respect to the degree of choice which a customer can exercise with respect to designing the structure and benefits of the policy.

There are two areas where customers may actively participate in this regard• While fixing and altering the structure of premiums and benefits

• While choosing how to invest the premium proceeds

4. The appeal – Needs met

The major sources of appeal of the new genre of products that emerged worldwide are given below:

a) Direct linkage with the investment gains: First of all, there was the prospect of direct linkage with the investment gains which life insurance companies could make through investment in a buoyant and promising capital market. One of the most important arguments in support of investment linked insurance policies has been that, even though in the short run, there may be some ups and downs in the equity markets the returns from these markets would, in the longer run, be much higher than that of other secured fixed income instruments. Life insurers who are able to efficiently manage their investment portfolios could generate superior returns for their customers and thus develop high value products.

b) Inflation beating returns: The importance of yield also stems from the impact of inflation on savings. As we all know, inflation can erode the purchasing power of one’s wealth so that, if a rupee today would be worth only 30 paisa after fifteen years, a principal of Rs. 100 today would need to grow to at least Rs. 300 in fifteen years in order to be worth what it is today. This means that the rate of yield on a life insurance policy must be significantly higher than the rate of inflation. This is where investment linked insurance policies were especially able to score over traditional life insurance policies.

c) Flexibility: A third reason for their appeal was their flexibility.

Policyholders could now decide within limits, the amount of premium they wanted to pay and vary the amount of death benefits and cash values. In investment linked products, they also had the choice of

investments and could also decide the mix of funds in which they wanted to have the proceeds of their premiums invested. This implied that policyholders could have a greater control over their investment in life insurance.

d) Surrender value: Finally, the policies also allowed the policyholders to withdraw from the schemes after a specified initial period of years (say three to five), after deduction of a nominal surrender charge. The amount available on such surrender or encashment before the full term of the policy was much higher than the surrender values available under erstwhile traditional policies.

These policies became very popular and even began to replace traditional products in many countries, including India because they were meeting a critical motive of many investors – the wealth accumulation motive which generated a demand for efficient investment vehicles. In the United States for example, products like “Universal Life” provided the means to pass on the benefits of high current interest rates returns which life insurers earned in money and capital markets very quickly to policyholders.

Flexibility of premiums and face amount meanwhile enabled the policyholder to adjust the premiums to suit his or her particular situations. The convenience of early withdrawal without undue loss also meant that the policyholder no longer needed to lock his or her money for long periods of time.

Which among the following is a non-traditional life insurance product?

I. Term assurance

II. Universal life insurance

III. Endowment insurance

IV. Whole life insurance

1. Some non-traditional products

In the remaining paragraphs of this chapter we shall discuss some of the non- traditional products which have emerged in the Indian market and elsewhere.

a) Universal life

Universal life insurance is a policy that was introduced in the United States in 1979 and quickly grew to become very popular by the first half of the eighties.

As per the IRDA Circular of November 2010, “All Universal Life products shall be known as Variable Insurance Products (VIP)”.

Universal life insurance is a form of permanent life insurance characterised by its flexible premiums, flexible face amount and death benefit amounts, and the unbundling of its pricing factors. While traditional cash value policies require a specific gross or office premium to be paid periodically in order to keep the contract in force, universal life policies allow the policyholder within limits, to decide the amount of premiums he or she wants to pay for the coverage. Larger the size of the premium, greater the coverage provided and greater the policy’s cash value.

The major innovation of universal life insurance was the introduction of completely flexible premiums after the first policy year. One had only to ensure that premiums as a whole were enough to cover the costs of maintaining the policy. What this implied is that the policy could be deemed to be in force, so long as its cash value was sufficient to pay the mortality charges and expenses.

Premium flexibility allowed the policyholder to make additional premiums above the target amount. It also allowed one to skip premium payments or make payments that were lower than the target amount.

Flexibility of structures also enabled the policyholder to make partial withdrawals from the cash value that was available, without the obligation to repay this amount or pay any interest on it. The cash value was simply reduced to that extent.

Flexibility also meant that the death benefits could be adjusted and the face amounts could be varied.

However this kind of policy could be mis-sold. Indeed, in markets like the US, prospective customers were enticed by the proviso that ‘one needed to make only a few initial premium payments and then the policy would take care of itself’. What they did not disclose was that cash values could maintain and keep the policy in force only if investment returns were adequate for the purpose. The decline of investment returns during latter half of the eighties led to erosion of cash values. Policyholders who failed to continue premium payments were shocked to find that their policies had lapsed and they no longer had any life insurance protection.

Diagram 1: Non-traditional life insurance products

In India, as per the IRDA norms, there are thus only two kinds of non-traditional savings life insurance products that are permitted:

• Variable insurance plans

• Unit linked insurance plans

i. Variable life insurance

To begin with it would be useful to know about variable life insurance as introduced in the United States and other markets.

This policy was first introduced in the United States in 1977. Variable life insurance is a kind of “Whole Life” policy where the death benefit and cash value of the policy fluctuates according to the investment performance of a special investment account into which premiums are credited. The policy thus provides no guarantees with respect to either the interest rate or minimum cash value. Theoretically the cash value can go down to zero, in which case the policy would terminate.

The difference with traditional cash value policies is obvious. A traditional cash value policy has a face amount that remains level throughout the policy term. The cash value grows with premiums and interest earnings at a specified rate. Assets backing the policy reserves form part of a general investment account in which the insurer maintains the funds of its guaranteed products. These assets are placed in a portfolio of secured investments. The insurer can thus expect to earn a sturdy rate of return on the assets in this account.

In contrast, assets representing the policy reserves of a variable life insurance policy are placed in a separate fund that do not form part of its general investment account. In the US this was termed as a separate account while in Canada it was termed as a segregated account. Most variable policies permitted policyholders to select from among several separate accounts and to change their selection at least once a year.

In sum, here is a policy in which the cash values are funded by separate accounts of the life insurance company, and death benefits and cash values vary to reflect investment experience. The policy also provides a minimum death benefit guarantee for which the mortality and expense risks are borne by the insurance company. The premiums are fixed as under traditional whole life. The principal difference with traditional whole life policies is thus in the investment factor.

Variable life policies have become the preferred option for those who wanted to keep their assets invested in an assortment of funds of their choice and also wanted to directly benefit from favourable investment performance of their portfolio. A prime condition for their purchase is that the purchaser must be able and willing to bear the investment risk on the policy. This implies that variable life policies should be typically bought by people who are knowledgeable and quite comfortable with equity / debt investments and market volatility. Obviously, its popularity would depend on investment market conditions – thriving in market booms and declining when stock and bond prices plummet. This volatility has to be kept in mind while marketing variable life.

ii. Unit linked insurance

Unit linked plans, also known as ULIP’s emerged as one of the most popular and significant products, displacing traditional plans in many markets. These plans were introduced in UK, in a situation of substantial investments that life insurance companies made in ordinary equity shares and the large capital gains and profits they made as a result. A need was felt for having both greater investment in equities and also passing the benefits to policyholders in a more efficient and equitable manner.

Conventional with profit (participating) policies offer some linkage to the life office’s investment performance. The linkage however is not direct. The policyholder’s bonus depends on periodic (usually annual) valuation of assets and liabilities and resultant surplus declared, which in turn depends on assumptions and factors considered by the valuation actuary.

Critical to the valuation process is the allowance for guarantees provided under the contract. As a result the bonus does not directly reflect the value of the underlying assets of the insurer. Even after the surplus is declared, the life insurer may still not allocate it to bonus but may decide to build free assets which can be used for growth and expansion.

Because of all this, bonus additions to policies follow investment performance in a very cushioned and distant manner.

The basic logic that governs conventional policies is to smooth investment returns over time. While terminal bonuses and compound bonuses have enabled policyholders to enjoy a larger slice of benefits of equity and other high yield investments, they are still dependent on the discretion of the life office who declares these bonuses. Again, bonuses are generally only declared once a year since the valuation is done only on annual basis. Returns would thus not reflect the daily fluctuations in the value of assets.

Unit linked policies help to overcome both the above limitations. The benefits under these contracts are wholly or partially determined by the value of units credited to the policyholder’s account at the date when payment is due.

Unit linked policies thus provide the means for directly and immediately cashing on the benefits of a life insurer’s investment performance. The units are usually those of a specified authorised unit trust or a segregated (internal) fund managed by the company. Units may be purchased by payment of a single premium or via regular premium payments.

In the United Kingdom and other markets these policies were developed and positioned as investment vehicles with an attached insurance component. Their structure differs significantly from that of conventional cash value contracts. The latter, as we have said, are bundled. They are opaque with regard to their term, expenses and savings components. Unit linked contracts, in contrast, are unbundled. Their structure is transparent with the charges to pay for the insurance and expenses component being clearly specified.

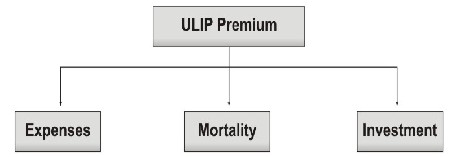

Diagram 2: Premium break-up

Once these charges are deducted from the premium, the balance of the account and income from it is invested in units. The value of these units is fixed with reference to some pre-determined index of performance.

Policyholder benefits thus do not depend on the assumptions and discretion of the life insurance company.

An endearing feature of unit linked policies is its facility of choosing between different kinds of funds, which the unit holder can exercise. Each fund has a different portfolio mix of assets. The investor thus gets to choose between a broad option of debt, balanced and equity funds. A debt fund implies investment of most of one’s premiums in debt securities like gilts and bonds. An equity fund would imply that units are predominantly in equity form. Even within these broad categories there may be other types of options.

Equity Fund |

Debt Fund |

Balanced Fund |

Money Market Fund |

This fund invests major portion of the oney in equity and equity related instruments. |

This fund invests major portion of the money in overnment Bonds, Corporate Bonds, Fixed Deposits etc. |

This fund invests in a mix of equity and debt instruments. |

This fund invests money mainly in instruments such as Treasury Bills, Certificates of Deposit, Commercial Paper etc. |

One may choose between a growth fund, predominantly invested in growth stocks, or a balanced fund, which balances need for income with capital gain. One may also choose sectoral funds, which invest only in certain sectors and industries. Each option that is selected must reflect one’s risk profile and investment need. There is also provision to switch from one kind of fund to another if performance of one or more funds is not perceived to be up to the mark.

All these choices also carry a qualification. The life insurer, while being expected to manage an efficient portfolio, does not give any guarantee about unit values. It is thus relieved here of the greater part of the investment risk. The latter is borne by the unit holder. The life insurer may however bear the mortality and expense risk.

Again, unlike conventional plans, unit linked policies work on a minimum premium basis and not on sum assured. The insured decides on the amount of premium he or she wishes to contribute at regular intervals. Insurance cover is a multiple of the premiums paid. The insured has a choice between higher and lower cover. The premium may consist of two components – the term component may be placed in a guaranteed fund (termed as the sterling fund in UK) that would yield a minimum amount of cover on death. The balance of premium is used to purchase units that are invested in the capital market, particularly the stock market, by the insurer. In case of death the death benefit would be the higher of the sum assured or the fund value standing to one’s account. The fund value is simply the unit price multiplied by the number of units in the individual’s account.

Which of the below statement is incorrect?

I. Variable life insurance is a temporary life insurance policy

II. Variable life insurance is a permanent life insurance policy

III. The policy has a cash value account

IV. The policy provides a minimum death benefit guarantee

• A critical point of concern with respect to life insurance policies has been the issue of giving a competitive rate of return which is comparable to that of other assets in the financial marketplace.

• Some of the trends that led to the upswing in non-traditional life products include unbundling, investment linkage and transparency.

• Universal life insurance is a form of permanent life insurance characterised by its flexible premiums, flexible face amount and death benefit amounts, and the unbundling of its pricing factors.

• Variable life insurance is a kind of “Whole Life” policy where death benefit and cash value of the policy fluctuates according to the investment performance of a special investment account into which premiums are credited.

• Unit linked plans, also known as ULIP’s emerged as one of the most popular and significant products, supplanting traditional plans in many markets.

• Unit linked policies provide the means for directly and immediately cashing on the benefits of a life insurer’s investment performance.

1. Universal life insurance

2. Variable life insurance

3. Unit linked insurance

4. Net asset value