This chapter aims to provide an understanding of the sales process and its various steps.

A. Sales process

Every one of us is engaged in selling almost from the day we were born. Each day we try to persuade, influence and induce one another to do (or not to do) things in the way we want. However this does not mean that we are all sales professionals.

Selling as a profession refers to the act of inducing a commercial transaction through inducing the purchase of a product or service, such act being carried out with the intent of earning remuneration.

The salesperson thus seeks to make a livelihood out of selling.

Insurance agents are sales persons who seek to induce members of the community to buy insurance contacts written by the insurance company that they represent. The remuneration they enjoy in return is known as a commission.

While all selling involves inducing someone to buy, the nature of the sales process can differ from industry to industry and would depend on the nature of the product and industry. The sales person’s role also consequently changes.

i. Fast Moving Consumer Goods (FMCG): are typically mass marketed through malls and other retail sales outlets. A product like soap, for example, is promoted through mass media (particularly ads in TV and other visual media) and the customer asks for it at a retail outlet (e.g. a shopkeeper or mall).

ii. Showroom sales: A car in a show room costs much more than a bar of soap and the buyer has to be naturally careful when taking a decision to buy. The sales person does not go to the prospect but instead it is the prospect who visits the showroom. The sales person has to win the prospective customer’s confidence and make a convincing case for purchase of the car. The role is essentially to convert an enquiry into a sale.

iii. Medicines and Drugs: are usually brought from a chemist after being prescribed by a doctor. Medical Representatives of pharmaceutical companies visit doctors’ clinics to sell their company’s products and their features to the doctor. Here the target of sales efforts is a medical expert who prescribes the brand for the end buyer who buys it from the pharmacy. The salesman’s role is basically sharing hard medical information with a professional.

iv. Business to Business (B2B sales): Here the customer is another firm. The decision to buy may be taken by multiple individuals and often it is a panel who decides. Purchase is typically through floating a tender and the selection criteria are fixed and measurable. Decisions are taken on the basis of careful consideration and evaluation of alternatives. The sales person’s role is to effectively demonstrate how the product and company meets the buying criteria better than the competition. It requires presentation skills, building good relations with multiple players and being sensitive to feedback and information that can help clinch the deal.

There are two points which distinguish life insurance selling from other products and industries:i. Firstly it is said that ‘life insurance is sold, not bought’. In case of many other products, the prospect has a need for the product and initiates the enquiry. In the case of life insurance, it is typically the sales person who has to go to the prospect and induces the need to buy.

ii. The second major difference is that in life insurance, unlike many other products, one is not selling any tangible product but only an idea – a promise that would be realised only in the future.

The role of the insurance salesman is to sell this promise and relate to the prospective customer in such a way as to win trust and confidence about the fulfilment of the promise far into the future. The element of person to person, eye to eye selling is perhaps far more in life insurance than any other business. It is one of the reasons why life insurance is considered difficult to sell. It is also for this reason that some of the world’s greatest and best known salesmen won their wings in the life insurance industry.

Selling is both an art and a science. It is an art in the sense that every sales person brings his own distinct style in the way he communicates, builds rapport and relations with prospective customers, engages in fact finding and presents solutions. Does this mean that only a few individuals who have these distinctive skills can succeed?

It is true that sales people may differ much in style and skills and their chances of success may vary. Some of them may be able to quickly make contacts with a lot of prospects and convert them effectively into customers in a short time. Others may be slower to learn and may move more slowly. The truth one needs to know is that so long as one does not give up or slacken but persists on the path, even when there are failures, the law of averages would come to one’s aid.

What is this law? It means that if a sales person on average is able to convert one out of every twenty or thirty persons contacted into a customer, he or she simply needs to adopt a standard process and keep contacting more and more

persons without giving up. The customer base will begin to build over time. Some sales persons may take longer than others but success is sure. Persistence is what pays off in the business.

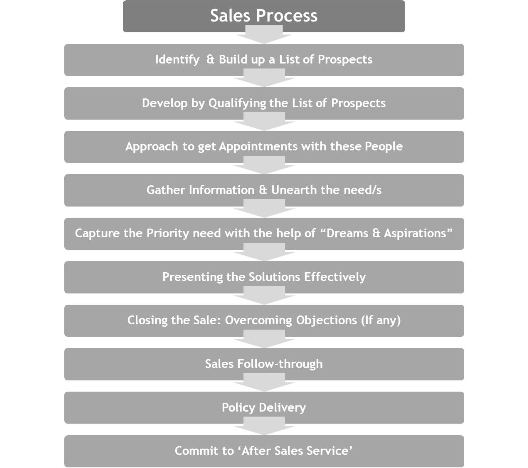

This brings us to the importance of adhering to a well-defined sales process with clearly sequenced steps. Let us outline the steps:

Let us look at each of these processes in some detail.

1. Step I: Prospecting (To identify and build up a list of prospects)

Prospects are people to whom we can sell our products. Prospecting is the process of gathering names of people whom one can approach to secure a sales interview. Continuous prospecting is absolutely vital to a successful sales career.

The key to effective prospecting is to target particular markets where we will be calling on people who have one or more characteristics in common. By cultivating strong relationships with these people, we can get them interested in the products we sell immediately, making the process of prospecting much

easier. Let us look at some of these markets.

a) Immediate group

The easiest people to approach would be one’s family and friends. We know the needs of these people and would be able to approach them on a favourable basis. Also relatively easy to approach are people with whom we do business; people who work in the food stores, clothing stores, banks, etc. Other such people would be those who know us such as friends, acquaintances, people who belong to the same organisations, and so forth. To sum up, these prospects form part of what we call the sales person’s natural market. They are people who should at least grant us an interview if we contact them.

b) Natural market

A second source of contacts is the natural market. This consists of people who may not be part of one’s immediate circle of relatives, friends and other acquaintances but one is in a position to know and get acquainted with them because of sharing something in common with these people. If we just look around we would see many groups who may form part of our natural markets:

• members of a caste or community association;

• members of a church congregation or a Satsang group;

• members of a parents – teachers association (PTA);

• members of a cultural association or a temple festival committee or a trade unionc) Centres of influence (COIs)

One way to get to a large number of prospects is by taking help from people who are visible and influential leaders and whose words are valued by others. We are referring to centres of influence – community leaders, social and political workers, professionals like Chartered Accountants or Lawyers or well-known businessmen.

The secret is to secure this person as a satisfied client whom you have served well and then to seek his or her help to find other new prospects. Even if he or she is not yet your client, it is enough he or she should know about your dedication and passion to help other people and should be confident about your knowledge and sense of professionalism. Another important condition is that he or she should like you and be interested in helping you.d) References, introductions and testimonials

Just as you can tap a centre of influence, you can also seek the help of other satisfied customers as well as prospects who has not yet bought or may not buy from you for some reason, but still has been impressed and favourably disposed to you by your dedication and professionalism.

i. A reference is a name of another potential prospect which is provided as a lead, by your client or prospect or centre of influence or any other person, whom you may be able to support with your solutions.

ii. Introduction: An even better way may be to ask for an introduction. Here the salesperson asks for a small letter of introduction or a note to the person referred. Typically one could ask for a visiting card at the back of which or attached to which, a small note may be added, introducing one to the referred person. The best form of introduction would off course be where one’s benefactor picks up the phone and calls his or her contact to introduce the agent, intimating that she would be contacting that person shortly. One’s chances of success would multiply, especially if the person who refers is one whose word is respected and taken seriously.

iii. A testimonial is a kind of statement which one may seek from a satisfied customer, affirming that the latter has done business with the salesperson and has been very satisfied with the services and solutions rendered. It is a kind of vouching for the sales person’s credentials. A testimonial would be very relevant when one is dealing with a circle of professionals who want adequate proof about the sales person’s professional credentials.e) Other service providers

There is a whole range of service providers who are not our competitors. They may include laundry men, real estate agents, lawyers, shop keepers, doctors and others whose services are regularly needed and sought by members of the lay public. The basic principle applied here is that of reciprocity. The agent agrees to be the eyes and ears for the other party, and in turn gets them to make her visible and recommended.

Good agents use this source very effectively. Indeed if were to make a visit to our milkman or laundryman, we may see a sign board asking one to contact so and so, with a contact number, for all one’s insurance needs.f) Conducting seminars and events

This is a professional, efficient method of selling, on a group basis. We can use it to attract both new and existing customers alike. Since we’re already dealing with existing customers, we can always ask them to invite a friend or partner along with them. Advertisements in the area of the seminar also can increase the numbers.

g) Information pieces, newsletters, blogs and web based networking

It may not be easy or even viable to conduct seminars and events on a regular basis.

i. Email

Another way to get your message and presence registered in the minds of a large number of prospects is to send them information by mail or hand drops on a regular basis. This can be done almost free of charge today in the form of e–mails.

ii. Newsletter

Another way to communicate regularly is through a newsletter. In both cases, the purpose is to inform readers about various subjects in the form of well-informed write ups. In designing newsletters you can involve some of your important customers and prospects, especially if their views are sought by members of their network.

iii. Personal website or blog

Yet another approach is to have a presence on the worldwide web in the form of a personal website. It may be a little expensive to begin with but it is a way for getting across to a wide circle of individuals who today spend a lot of their time in cyber space.

iv. Social networking sites

Finally there is Facebook and other social networking sites where you can access millions of others almost anywhere in the world.

h) Cold calling

This approach is used by many sales people in many different industries, not just financial services. This is where we make approaches to people or companies unannounced. It is tough and we have to able to accept rejection, but it can be a very quick way of gathering names and getting people to see. A good number of top sales people allocate some of their time to cold calling simply because it works.

i) A prospects’ file

It is most important that we establish a prospects’ file. This is simply a book or register or data base containing all the vital information about each of our prospects with details and date when the prospect should be called on. A prospects’ file is an ever-changing tool. New names must be added continuously on a daily basis and old names must be discarded if the individual is not receptive to our sales efforts. We must be sure that we have enough prospects to call on each day.

2. Step II: The pre-interview approach

Qualifying every prospect in the prospects’ list and getting appointments is the next step.

"Qualified" prospects are those people

• who can pay for insurance,

• who can pass the company underwriting requirements,

• who have one or more needs for insurance products, and

• who can be approached on a favourable basis

We need to gather enough meaningful information on each name in our prospect-list before we can call on them. The process is called qualifying the prospect.

The initial contact can be made through a letter, by telephone, or in a face-to- face meeting. Whatever method is used, the objective is the same: to get the prospect to consent to an interview where we can understand his or needs and in turn get an opportunity to explain the service that we have to offer.

In order to do this our pre-approach communication should include:

• Something that will arouse the prospect's interest

• Offering of a valuable service

• Making it clear that no commitment is being made

• Use of a third party influence, if possible

• Use of alternatives in order to get an affirmative response

• Obtaining a definite appointment

It is important that during our first contact with the client, we introduce ourselves in a manner that can generate rapport and also some trust and comfort feeling.

3. Step III: The sales interview: Conducting a need – gap analysis

After being successful in obtaining an interview, it is vital to do it in a systematic and professional manner. The first step is to make a proper approach which automatically and smoothly leads to the fact finding part of the sales interview. The approach basically consists of an introductory conversation in the course of which we are able to identify one or more needs of the prospect and get the latter to agree that these are significant needs for insurance protection. Once there is mutual agreement on these one can move forward.

In need gap analysis we engage in a process of gathering detailed information about the prospect’s insurance requirements, to identify and determine the assets and perils for which there is inadequate coverage. The objective here is to collect as much additional information about the prospect as possible. This additional information helps to identify specific needs of the prospect in a more cogent way, to suggest solutions to those needs, and to help the prospect find the money to pay the premiums.

In need analysis method we do the following things:

i. the present and the future needs of the family are analysed;

ii. the monetary value of these needs are then calculated;

iii. the difference between the funds so needed to meet these needs and the available fund with the family as at present is ascertained This difference is taken to be the required amount of risk cover.

Needs method takes account of the pressing needs of the family, showing how insurance can be added at various stages in the individual’s life as needs increase and income also improves. However the estimation of the potential estate of the insured, that we considered earlier when we talked about Human Life Value, is ignored here. The needs approach however makes selling easier.

The needs of the family can be enumerated as under:

i. Clean-up funds for medical expenses, funeral expenses, succession/inheritance expenses, outstanding loans etc.

ii. Readjustment income: enough income for permitting enough time to smoothly shift to a required adjustment in living conditions;

iii. Income for family: till children are self-supporting;

iv. Life income for spouse: after children become independent;

v. Special needs: mortgage redemption, emergency medical needs, marriage of daughter, and higher education of children etc.

The above broadly covers all the foreseeable needs and substantially defines the ambit that an insurance salesperson can address.

4. Step IV: Designing the solution

After completing the previous steps, we should know enough about the prospect to design and recommend a solution that is best for him or her at this point in time given all of his or her financial circumstances. In many cases, especially if the problems and solutions are of a simple nature, we would be able to recommend a solution and move on to closing the sale in one interview.

In other cases, where the situation is more complicated, we may need to spend some time in our office for developing the proper solution, then return to the prospect and make our recommendation in a second interview.

If we attempt to conduct the fact-finding session and present our solution all in one interview, we must be prepared to build a bridge from the fact-finding phase to the solution and recommendation phase. This requires identifying the prospect's most critical need, pointing out that need and getting an affirmative reaction from the prospect that this is indeed a very important need in his or her mind. We would then be in a position to present our prospect with a solution to the problem.

Typically one should conclude the initial fact finding interview with a promise to return soon with appropriate solutions to the prospect’s identified needs. One should then return to one’s office where one can analyse the prospect's problems in depth, design one or more solutions to these problems, prepare one’s proposals and recommendations which would lead to the sale, then make an appointment with the prospect for the second interview.

There is no specific rule which states the number of interviews one must have with the prospect. It will depend from case to case. There may be situations where you may have to conduct more interviews to develop a satisfactory solution and also win the prospect’s consent to listen to the solution and consider it.

5. Step V: Presenting the solution

The most important point to remember when presenting our solution is to be thoroughly prepared. Prior to making our proposal we would want to review the prospect's needs in detail, go over our solution one final time, and plan to make our presentation so that it will appeal to our prospect's buying motives. We would also want to anticipate what objections the prospect might raise to our proposal.

It is necessary to arrange for presenting our proposal to the prospect, at a time and place that will be free from interruptions and distractions. As we begin presenting our solution, we must put the prospect at ease while at the same time making sure that he or she understands that this is a decision-making session.

We need to begin by reviewing all the data we obtained in the fact-finding session and stating each of the prospect's problems in an affirmative manner. We must ensure we convey to our prospect that we have spent a lot of time reviewing his / her situation, and that we are quite confident our recommendations are the best possible solutions to these problems. It is very important that we relate each feature of our recommendation to some particular benefit which the prospect will gain from, if he or she buys our proposal. Rather than describing what we have to offer in technical terms, we should explain how the prospect will be getting what he or she wants and needs.

6. Step VI: Handling objections (if any) Diagram 3: Handling objections

The list of possible objections is a long one. It ranges from prospect being busy, not interested, thinks he has all the insurance he needs, already has an agent he deals with, has no money etc.

Finally there is the prospect who may agree with all that you say and have no objections, but decides to buy the product solutions from someone else. In all instances it means that the prospect does not have sufficient information to help him make the decision to buy from you.

If a prospect is “too busy now,” it means you have not provided information that could pique his interest or overcome his wariness of being ‘sold to’. Similarly the objection of “no money” can mean that he is not convinced adequately about why and how he can pay for the insurance. If he does not trust you, it is because you have not communicated enough information to overcome his doubts.

The least a salesperson can do is to accept and take responsibility for the fact that one has not adequately done the job of giving prospects the information they want to hear and see if there is anything one can do about it. Whatever the type of objection, we can handle it with this approach. The idea is not to treat it as a battle between us and the prospect where we win and they lose, but a discussion in which our sharing of what we know helps to convince them about the importance of meeting and buying from us.

a) Handling objections through LAPAC

One of the important techniques that one can use for handling objections is known as LAPAC (Listen, Acknowledge, Probe, Answer and Confirm). This method can be used to deal with objections at any stage of the sales process. It respects the prospect’s point of view, shows we are listening and persuades rather than attacks the prospect. Let us look at its elements:

i. Listen

Actively pay attention to all statements and gestures. This becomes important especially to know what the underlying concern is. Sometimes the prospect may need to be gently probed with questions to clarify the issue.

Example

What does the term ‘no money’ mean?

• Is it that there is no money now or

• Is it that the price is too high to buy it or

• Is it that the prospect does not feel that the money is worth spending?ii. Acknowledge

It is very important to affirm aloud so that both the prospect and the salesperson are on the same page. Acknowledgement is also linked to another very critical act, namely empathising with the prospect. Empathy does not mean that one necessarily agrees with the position taken by the other party. But it certainly means that one respects and tries to see it from the other person’s point of view.

Example

Once you are able to see the prospect’s reluctance to spend the money, you must express that you can see and understand how he feels. Probably you have faced a similar situation and some sharing on your part could demonstrate your understanding of what the other party is going through.

iii. Probe

This step is intended to seek more information about the prospect’s concern area. Remember that if the prospect has a problem in buying, that problem or set of problems have to be sorted out by the prospect himself, either by making a change in his thinking and mind-set or his action.

Example

If the prospect is too busy, he / she must find the time and inclination to meet you. If money is the problem, he / she needs to find ways to generate it.

Probing can do two things. If done in a counselling oriented and friendly manner, a set of gentle questions could guide the prospect towards finding answers to his / her own concerns. Probing can also help to elicit further details of the problem situation which causes the objection. Such information could be important and cannot be overlooked when one is answering the objection.iv. Answer

The task here is to obviously provide a carefully worded reply that suits the situation and is convincing to the prospect. Answers must be directed at and address the concerns that are raised. They must not be evasive or seek to deflect the concerns.

v. Confirm

The last step is to confirm whether the prospect is satisfied with the answer and if there is anything else needing to be known. If the body language and other signals make you feel that the prospect is not fully convinced, you may need to offer alternative options that he could consider. Getting this confirmation is very important because once a prospect says he / she is satisfied, the ground is laid for moving to the close of the sale.

7. Step VII: Closing the sale

Closing is the process of persuading the prospect to buy now. The key to successful closing lies in helping the prospect to want to say "yes".

We begin by summarising the presentation, making sure that the prospect understands exactly what the proposal is, and then leading the prospect into an affirmative answer. At this point, when we know that the prospect understands the proposal and is in an affirmative mood, we can conduct a definite close.

a) Closing methods

i. Implied consent

One approach often used is the "implied-consent" method. We simply start filling out the application asking a simple question such as "now, your last name is spelled as ". If the prospect does not stop us, the sale has probably been made.

ii. Offering alternatives

Another closing method is to offer the prospect an alternative between two minor decisions, either of which would lead to a close. For example, we may ask the prospect if she would prefer to make his payments once a year or twice a year. Here assumed consent is combined with a seemingly minor decision.

While making a close it is important that one should not try high pressured tactics to make a prospect buy something for which there is no real need or where the prospect cannot afford what is being recommended. Such practices of selling are unethical.

In other cases where we are persuading the prospect to take positive action, we must be aware that we are actually rendering an important service to the prospective customer, which the latter would eventually recognise and appreciate.

8. Step VIII: Sales follow-through

Between the time that the application is submitted and the policy is completed and delivered, the four most important responsibilities of the agent are to see that:

i. The application is clear, complete and accurate

ii. Being actively involved in making sure that any further investigations that are required gets completed in a convenient and timely manner

iii. The client's advisors, such as accountants or attorneys, are treated in the same manner that our client is treated and that we do not invade their areas of expertise, and

iv. That all questions and requests are promptly followed up

9. Step IX: Policy delivery

Delivering the policy is an extremely important step in the insurance sales cycle. It provides the agent with the opportunity to perform four important functions:

i. To resell and reaffirm the need

ii. To get the client thinking about the next purchase

iii. To get referrals and

iv. To build prestigea) Policy delivery procedure

As with the sales process, a proper policy delivery requires a structured, step- by-step procedure such as:

i. Check the entire policy for accuracy

ii. Prepare the policy and the policy wallet, if available

iii. Telephone the client for an appointment

iv. Thoroughly prepare for the delivery interview

v. Congratulate the client for purchasing the insurance

vi. Explain the features, advantages, and benefits of the policy. Relate all benefits to the client's actual situation using names of family members, motivational stories, etc.

vii. Prepare the client for the next sale. Remind the client of the needs that have not yet been covered. Tell him or her of the need to periodically review these

viii. Commit sincerely to the client's service. Tell the client we will contact him / her regularly and that he / she should call us immediately if there are any questions or problems

ix. Ask the client for referred leads

10. Step X: Commitment to service

Service on the part of the agent is an integral element of the sales cycle. Essential to a commitment to service is a structured program for maintaining contact with our clients. Such a program could consist of:

a) Conveying clearly

At the time of the policy delivery, we need to make a service commitment to our client. We should tell the client that at least once a year we will call to carefully review his / her insurance program. Many good agents set the exact date for this service call before leaving the delivery interview.

b) Committing to continuous contact

Throughout the year a good agent should keep in touch with the client in as many ways as possible. The agent may want to send greeting cards on birthdays, wedding anniversaries, etc. A small gift that is personal and useful may be sent from time to time. Newspaper clippings, insurance related items, picture postcards when on trips, are all tokens of the agent's thoughtfulness and may be sent to the client on a random basis.

c) Annual service review plan

At least once a year, one must schedule an annual service review with the client. We should schedule this service call well in advance. During the annual service review, one can take the opportunity to remind the client why he / she purchased his / her latest policy, may discuss any needs of the client which are yet unfulfilled, and if appropriate, can suggest to the client that additional insurance be purchased at this time to cover his / her outstanding needs.

Persistency

One of the important reasons for having a proper sales and service follow up is to ensure that the policy holder continues to keep the policy in force through regular payment of premiums.

Persistency may be defined by the percentage of policies / premiums introduced in a certain year that have been renewed in subsequent years.

It is observed that most policies which lapsed and are not renewed do so within the first three years. When policies lapse the company loses, because the heavy costs that have been incurred at the time of acquiring new business may not have been recovered. More significantly, low persistency is also often a symptom of dissatisfaction and loss of confidence of the insured with the insurer. If the agent does not take care of his or her client, both during the sales and post sales stages, such dissatisfaction can soon lead to loss of credibility of both the agent and the company he or she represents. Hence it is very necessary to carefully monitor persistency rates as it is a sure sign of the health of the company.

The importance of continuous service cannot be overemphasised. It is one of the critical keys to high persistency. We, particularly in insurance sales, always need to remember that while our purpose is to provide a need based solution to the customers we must also sincerely commit to a continuous service that cannot be matched by any other competitor.

Which of the below statement best describes a “testimonial”?

I. An endorsement from a satisfied customer

II. Test result for a product in a benchmarking test

III. List of tests that a product must pass

IV. Money required to test a product

• Selling as a profession refers to the act of inducing a commercial transaction through inducing the purchase of a product or service, such act being carried out with the intent of earning remuneration.

• Insurance agents are sales persons who seek to induce members of the community to buy insurance contacts written by the insurance company that they represent.

• Prospecting is the process of gathering names of people who can be approached for a sales interview.

• Target markets for prospecting include:• Immediate group

• Natural market

• Centres of influence

• References, introductions and testimonials

• Other service providers• A professional, efficient method of selling on a group basis includes conducting seminars and events.

• An easy and viable means of reaching out to prospects on a mass scale include emails, newsletters, personal website or blog, social networking websites etc.

• "Qualified" prospects are those people:• who can pay for insurance,

• who can pass the company underwriting requirements,

• who have one or more needs for insurance products, and

• who can be approached on a favourable basis• During a sales interview with the prospect; the agent should do a need – gap analysis

• In need gap analysis we engage in a process of gathering detailed information about the prospect’s insurance requirements, to identify and determine the assets and perils for which there is inadequate coverage.

• After completing the sales interview successfully, the agent should design a solution based on the prospect’s need and present the solution.

• The agent may handle client objections using the LAPAC (Listen, Acknowledge, Probe, Answer and Confirm) approach.

• Closing a sale involves persuading the prospect to buy now. While closing the agent may use the ‘implied consent’ method or offer alternatives to the prospect.

• Once the sale is closed, the agent should do a sale follow-through and deliver the policy

• Service on the part of the agent is an integral element of the sales cycle. Essential to a commitment to service is a structured program for maintaining contact with our clients.

1. Selling as a profession

2. Sales process

3. Prospecting

4. Natural market

5. Centres of influence

6. Reference

7. Testimonial

8. Qualified prospects

9. Need-gap analysis

10. LAPAC (Listen, Acknowledge, Probe, Answer and Confirm)

11. Closing

12. Implied consent